Parents

Research

Mar 11, 2026

Like Space Itself, the Satellite Industry is Unbounded

Andrew Z

Research Fellow

Like Space Itself, the Satellite Industry is Unbounded

A Shining Star in Space

The space economy, comprising all the businesses and activities that involve space such as building and launching rockets, making satellites, operating space-based services like GPS, etc. generated roughly $415 billion in revenue in 2024. Most of this money came from commercial satellites, which brought in about $293 billion and made up 71% of the entire space economy. This shows that the biggest driver of space growth isn’t astronauts landing on the Moon or robots exploring Mars—it’s the thousands of small satellites quietly orbiting Earth every day.

Looking ahead, the space economy is expected to grow even faster. By 2035, it could reach around $1.8 trillion. Even under conservative assumptions, the satellite market alone is projected to grow to about $108 billion, up from roughly $15 billion today. This means satellites are likely to be one of the most important growth engines in the entire space industry. In 2024 alone, there were 259 orbital launches, sending nearly 2,700 satellites into space. The United States has been a major beneficiary of this trend, accounting for about 65% of global launches and 69% of satellite manufacturing.

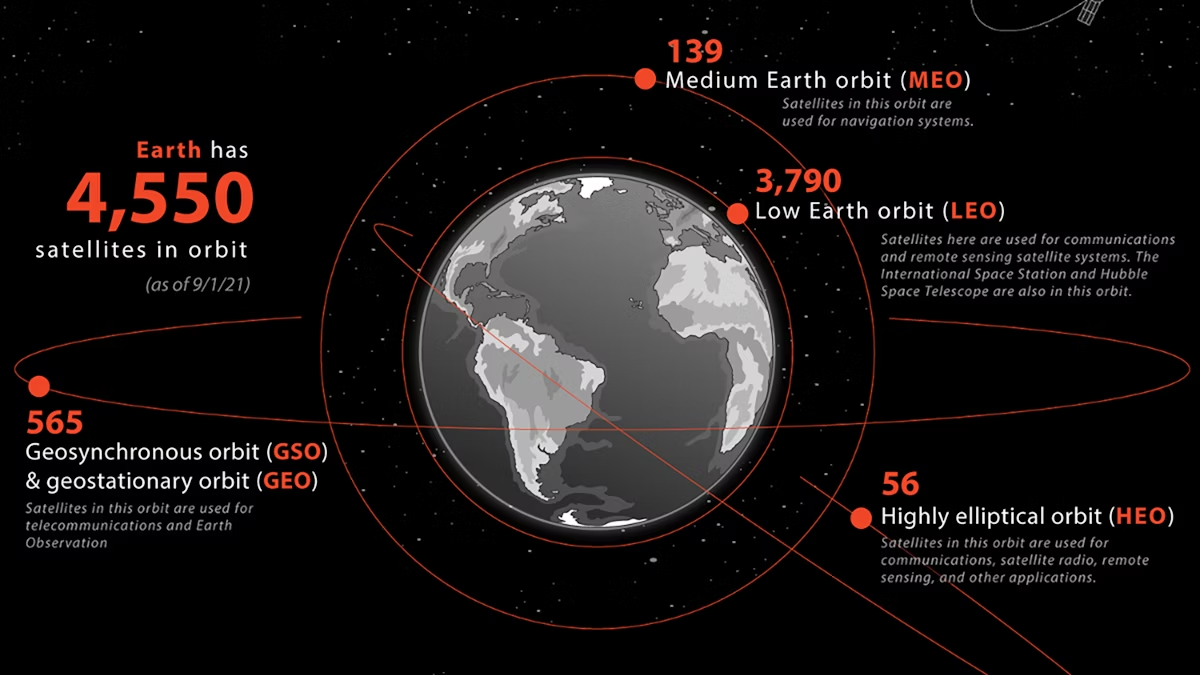

Of the more than 4,000 satellites currently in orbit, the majority (over 3,000) operate in low Earth orbit (LEO). LEO satellites are typically installed at altitudes of 100-1,200 miles and complete an orbit of the Earth roughly every 90 minutes. Satellite launches are increasing at an extremely fast pace—faster than the rate described by Moore’s Law, which is often used to explain how quickly computing power improves. Approximately 70,000 additional LEO satellites are expected to be launched over the next five years.

Source: Dewesoft

The rapid expansion in satellite deployment is already evident. More importantly, three trends are beginning to define the next phase of the satellite industry, particularly in low Earth orbit (LEO), including falling launch costs, improving satellite performance, and intensifying competition. All of these should warrant the attention of retail investors.

Time to Fly

The first major driver of future satellite growth is more efficient launch technology. Satellites are sent into space using rockets, and historically, this cost of placing satellites into orbit was the single greatest constraint on industry growth. However, as rocket technology improves and rockets are able to carry larger payloads, the cost of launching a kilogram into LEO could, in theory, fall to $100-200. While these numbers represent long-term potential rather than today’s average prices, costs have already dropped dramatically.

The main reason for this cost decline is rocket reusability. Modern reusable rockets can be launched, landed, and flown again, spreading fixed costs across many missions. This makes it possible to launch dozens of satellites at once, sometimes around 60 LEO satellites in a single launch, which lowers the cost per satellite. SpaceX is a clear example of this trend. In August 2025, Starship test launch 10 was successful in deploying starlink satellites and reusing the new Super Heavy booster with increasing reliability. Starship's estimated launch costs are approaching $100 per kilogram and with the expectation of launching 100 starlink satellites per launch.

Launch costs are also falling because companies are developing satellite-servicing spacecraft: specialized vehicles equipped with robotics, autonomous navigation, and advanced software that allow satellites to be repaired, refueled, repositioned or safely deorbited instead of being replaced. Extending the life of satellites reduces the need for constant new launches, lowering overall system costs. Since 2020, Northrop Grumman's SpaceLogistics Mission Extension Vehicles have successfully prolonged the operational lives of two Intelsat geostationary communications satellites. A more advanced system, the multi-armed Mission Robotic Vehicle, is scheduled to launch in early 2026. On the private side, in 2024, Starfish Space raised $29 million to develop autonomous vehicles for life-extension in geostationary orbit and debris removal from LEO, aiming to build the lowest-cost satellite-servicing architecture possible.

How Can I Live Without Wifi?

Low Earth Orbit satellites represent the latest generation of internet-providing infrastructure. These satellites are mass-produced, with unit costs as low as $7,000 per satellite before launch costs are added. Because they orbit much closer to Earth, LEO satellites can deliver fast internet speeds with very low delay, often between 2 and 27 milliseconds. This performance makes satellite internet a realistic alternative to both home broadband and mobile wireless networks.

The shift toward satellite-based internet has also been made possible by major advances in antenna technology. Older satellite internet relied on large, dish-shaped antennas that had to physically move to point at a satellite, which does not work well with fast-moving LEO satellites. New Electronically Steered Antennas (ESAs) solve this problem. These antennas are small, flat—about the size of a pizza box—and solid-state, meaning they have no moving parts. Instead of rotating mechanically, they use electronics to instantly steer signals and track satellites as they race across the sky. This allows the antenna to track fast-moving LEO satellites smoothly and continuously, even as one satellite moves out of range and another takes its place, making satellite internet reliable not only for homes and businesses, but also on moving ships, airplanes, trains, and vehicles, where traditional antennas would fail.

Taking this application further, satellite internet works in any place where traditional infrastructure does not, including remote or rural regions that lack fiber-optic cables or cellular towers. They also play a crucial role during natural disasters or conflicts, when ground-based networks are damaged or shut down. This means that in the coming years LEO satellites can provide data where none exists, the most imminent users of which draw from the currently 2.5 billion people, or 31% of the global population, that still lack internet access.

Source: Gravity Internet

I Want It, No I Want It

And as always, competition drives innovation. In the US, the White House has requested about $40 billion for the US Space Force. At the same time, other countries—especially China and Europe—are also investing heavily in their own space programs. These rising defense budgets create major opportunities for satellite companies. For example, proposals like Golden Dome, a planned multi-layered missile defense system, rely heavily on satellites to detect and track threats. This demand is already translating into real contracts. The Space Development Agency (SDA) has announced $3.5 billion in contracts awarded to four companies to build the next phase of a LEO satellite network designed to detect and track advanced missiles.

Satellite companies also understand that while space may look endless, the best orbits are limited. Certain altitudes work better than others because they offer the right balance of coverage, speed, and visibility. Because these prime orbits are scarce, companies are racing to launch satellites and secure regulatory approval, accelerating launch filings with the International Telecommunication Union in order to secure spectrum and orbital priority. Those benefits push firms to deploy even faster and at a larger scale, accelerating the overall growth of satellite networks.

What to Consider

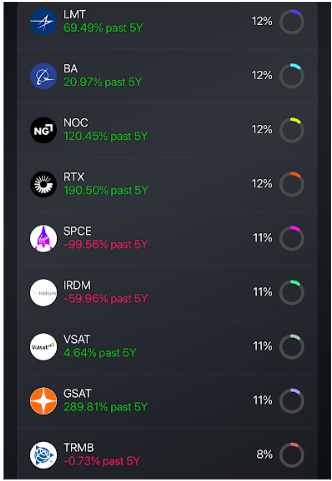

The US space industry attracts more private investment than any other country, accounting for 52% of all private investment in space worldwide. Most of this money is focused on just a few companies. Around 80% of venture capital funding goes to SpaceX, while the remaining 20% is spread across only three or four other major companies, each typically valued between $500 million and $2 billion.

Because so much investment is concentrated in private startups, it has historically been hard for everyday investors to gain exposure to the space industry. However, that is starting to change. While many of the biggest space companies are still privately owned, retail investors can now gain access through publicly traded companies, including defense contractors, infrastructure providers, and space-focused investment funds.

While much of the value creation in the satellite industry still happens in private companies, retail investors can gain meaningful exposure through public markets. As satellite usage expands across defense, communications, and broadband based on the trends outlined above, retail investors should definitely be interested. You may consider:

- Defense & aerospace primes driving government satellite spending:

- Lockheed Martin (LMT)

- Boeing (BA)

- Northrop Grumman (NOC)

- RTX (RTX)

- Space-infrastructure builders enabling launch, deployment & orbital expansion:

- Maxar (MAXR

- SpaceX proxy via Virgin Galactic (SPCE)

- Satellite operators delivering real-time data, broadband, & communications:

- Iridium Communications (IRDM)

- Viasat (VSAT)

- Globalstar (GSAT)

- Supporting software and calibration tools that rely on satellites to localize objects in real time:

- Trimble (TRMB)

And you can get invested in these through a custom portfolio created by Bloom:

Disclosure: This material is provided for informational purposes only and is not intended to constitute, and should not be relied upon as, investment advice, a recommendation, or a solicitation to buy or sell any securities. Nothing contained herein is intended to be, or should be construed as, an offer to sell or a solicitation of an offer to purchase any security or investment product. Any investment decisions should be made only after careful consideration of the applicable risks and, where appropriate, consultation with qualified financial, legal, or tax professionals.